We were delighted to hold a webinar last Wednesday 19th July, on the new UK Mortgage Charter and its implications on Interest Rate Risk, which was well attended by over 60 banking institutions. Luke & Joe DiRollo from ALMIS® International were joined by IRRBB expert Paul Newson.

The UK Mortgage Charter, which took effect this month, and was jointly confirmed and implemented by the Financial Conduct Authority and the UK’s principal mortgage lenders, serves the crucial purpose of providing reassurance and support to borrowers amid uncertain economic conditions and high-interest rates. During our webinar, our panellists unanimously agreed that the Charter brings about challenges for both the prudential regulator and fixed-rate lenders.

Of particular significance are two key agreements outlined in the Charter.

Firstly, qualifying repayment mortgage customers now have the option to switch to interest-only payments for a period of 6 months or extend their mortgage terms to reduce their monthly payments. Our expert, Paul, pointed out that lenders have been encouraged to support this for longer durations, similar to the Covid support schemes. Additionally, by net-hedging repricing mismatches, changes in repayment structures due to this option could be more effectively managed and supported. Our panel highlighted that institutions should also consider the wider credit risk implications of assisting these customers and explore ways to provide further support.

However, the second agreement, which comprises two terms, raised concerns among our panellists. This agreement allows customers approaching the end of a fixed-rate deal to lock in a new deal up to six months in advance, granting them the flexibility to either proceed with the new deal or request better like-for-like products if rates fall. This “loose-loose” scenario poses challenges for lenders, as Joe explained. Decisions on hedging pipeline at acceptance are crucial and involve inherent risks. Hedging less than the full amount could lead to losses if rates rise, while hedging more than the full amount may result in a higher-than-market-rate hedge for the loan period. While this agreement doesn’t necessarily change the mechanics of fixed-rate lending, it exacerbates a free and valuable customer option that the market has considered necessary to compete. The FCA, together with other financial advisers, will encourage customers to exercise this option when suitable. Furthermore, we are now seeing an extension of this option from around 3 months to 6 months. Effectively, borrowers are better informed, the option duration is longer and market volatility is higher. All three of these components heighten the interest rate risk implications for lenders.

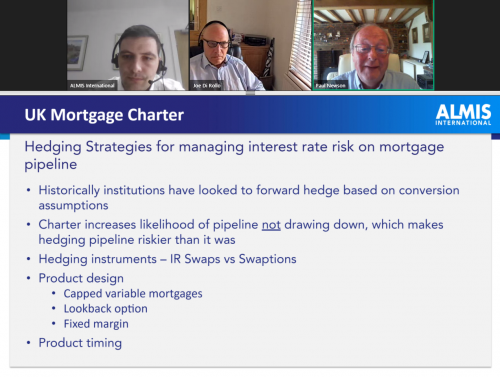

To address this, our panellists highlighted the importance of quantifying this risk should institutions engage in fixed-rate pipeline and the following approach was recommended for this:

- Compute repricing gap pre hedge given contractual position of pipeline.

- Decide and implement a hedging strategy based on behavioural assumptions.

- Forecast balance sheet forward using multiple behavioural scenarios (e.g. expected, -3% and +3% scenario).

- Run value/income sensitivity on the multiple behavioural scenarios based on hedging strategy.

During the webinar, we polled an audience of over 140 treasury professionals, revealing that 59% hedged fixed-rate loans on written offer, while 31% and 10% hedged on product launch and completion, respectively. In a typical scenario, 76% of attendees expected 51-75% of the pipeline to drawdown, with 24% expecting 76-100% conversion. Attendees did suggest that, in a stress scenario of a 3% fall in rates, 10-30% of pipeline would drawdown.

As the Charter increases the likelihood of pipeline not drawing down, hedging pipeline risk becomes riskier than before. However, our panellists unanimously agreed that forward hedging remains an optimal strategy. While the market has floated the idea of swaptions, they can compromise the commercial viability of mortgage products. Our experts, Paul and Joe, presented medium-term alternatives, such as capped variable mortgages and lookback options, to address these challenges. The discussion also covered the importance of product timing and how institutions should manage their offers in alignment with pipeline volumes, considering that introducing cheaper products could impact profitability.

As experts in treasury and ALM, we really enjoyed hosting this topical webinar and providing valuable insights into the implications of the UK Mortgage Charter on Interest Rate Risk. Stay tuned for more thought-provoking events and discussions from our team. Thank you to all who joined us and participated, and we look forward to continuing to lead the conversation on crucial financial topics.

If you have any more questions on this, or if you are interested in viewing a recording of the session and/or to see the presentation slides, please email us.