In this article, we review the Bank of England’s Call to reduce data risk by enhancing regulatory reporting controls and increasing data lineage and data quality.

The recent communication to banking executives, the Bank of England (BoE) highlighted persistent challenges in regulatory reporting, underscoring the importance of robust data governance, accuracy and data lineage. This Dear CEO letter, part of an ongoing initiative to enhance banking supervision, casts a spotlight on the need for improved data management within financial institutions.

The letter outlines deficiencies identified through a comprehensive program of skilled persons reviews. These reviews, encompassing a significant sample of firms, have repeatedly uncovered lapses in data controls, governance, systems, and production controls associated with regulatory reporting.

The BoE emphasises that the submission of complete, timely, and accurate regulatory returns is fundamental to effective supervision. The message is clear, banks should take heed the feedback and undertake necessary remedial actions.

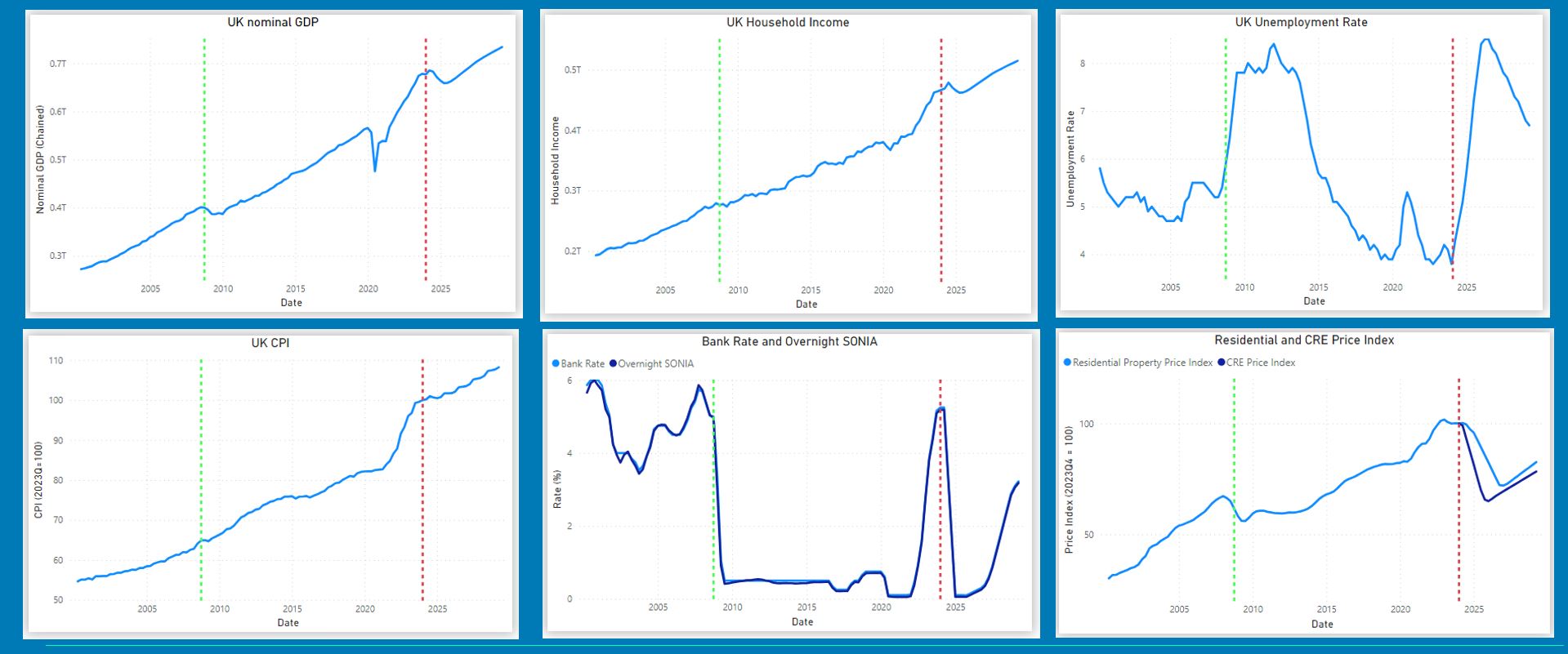

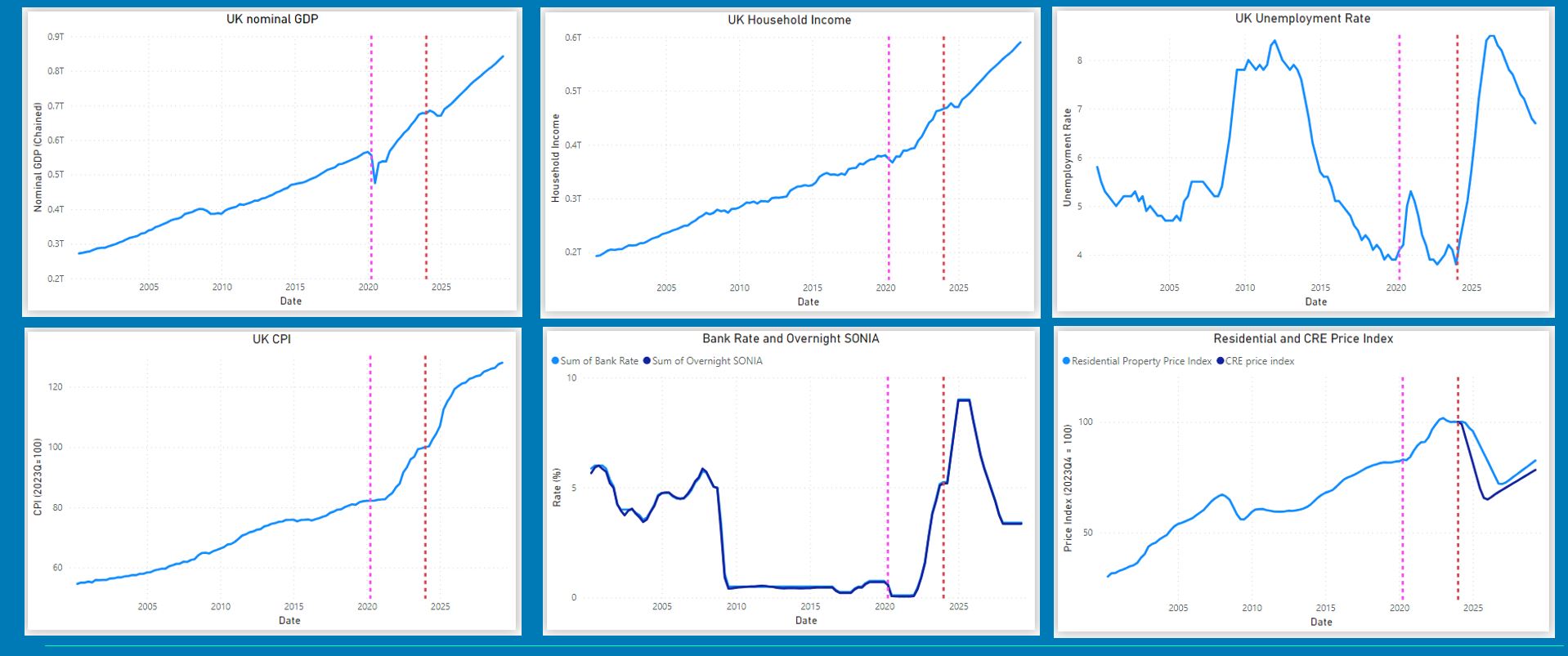

A key aspect of ensuring data accuracy and governance is maintaining robust data lineage. Data lineage tracks the flow of data from its origin through various transformations to its final state, providing transparency and accountability. This capability allows practitioners to stand confidently behind the reports produced, ensuring that every data point is traceable and verifiable.

At ALMIS® International, we’ve tackled the challenge head on with recent developments to our bank treasury data warehouse and reporting applications. All data enrichments and changes are logged per transaction with drilldown back to transaction-level accounts.

As regulatory scrutiny intensifies, the BoE is set to continue deploying targeted supervisory tools, including the use of skilled persons, throughout 2024. This proactive stance reflects a broader industry concern about the adequacy of risk data aggregation practices, as highlighted in the Basel Committee on Banking Supervision’s (BCBS) recent progress report on the adoption of BCBS 239 standards. The report reveals that significant work remains to ensure that data accuracy and risk data aggregation are prioritised across all data types.

The Bank of England’s letter also signals forthcoming long-term reforms through its Transforming Data Collection Programme and the PRA’s Banking Data Review. These initiatives aim to overhaul how data is collected, and which data points are prioritised, ensuring a more streamlined and effective regulatory reporting framework. There are three key industry reforms banks will need to consider;

- Defining and adopting common data standards that identify and describe data in a consistent way throughout the financial sector.

- Modernising reporting instructions to improve how our reporting instructions are written, interpreted and implemented.

- Integrating reporting to move to a more streamlined, efficient approach to data collection.

As the BoE and other regulatory bodies intensify their focus on data management, the message is clear: data accuracy, governance, and lineage must be at the forefront of their operational priorities. As regulatory bodies tighten their oversight, financial institutions are urged to invest in their data management systems, ensuring that their regulatory submissions meet the high standards expected by supervisors. Engaging with the ongoing reforms and industry forums will be crucial for banks to navigate this evolving regulatory landscape effectively, whilst balancing the cost of compliance with operational efficiency.

About the Author

Matt Poole is an experienced CertBALM-qualified Product Owner at ALMIS® International specialising in data warehousing and banking risk calculations for treasury, ALM, and regulatory reporting.

ALMIS® International has a team of experts in bank Asset Liability Management, Regulatory Reporting, Hedge Accounting and Treasury Management supporting over 65 Financial Institutions. Please get in touch to learn more about how we can help